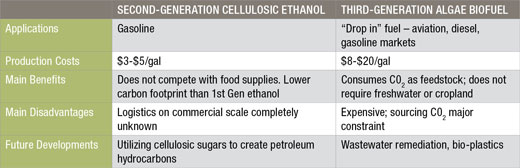

Biofuels 2010: Spotting the Next WaveMay 25, 2010 - gtmresearch.com The Economics of Biofuels Point to Near-Term Opportunities for Cellulosic Ethanol and Long-Term Ascendancy of Algal BiofuelsThe Prometheus Institute, having elevated the discussion of solar power to one rooted firmly in economics with the publication of the book The Solar Revolution, has turned its attention to biofuels with this groundbreaking new market study. Through a rigorous economic analysis of all current and proposed generations of biofuels, authors Joshua Kagan and Travis Bradford chart a clear path forward for future biofuels over the next 13 years, with forecasts for a firm establishment of a diverse biofuels industry globally and significant growth for algae biofuels. IntroductionBiofuels have been in existence since the 1970s. Prior to 2010, every global commercial biofuel plant was either for first-generation ethanol or biodiesel. Biofuels are an inherently local proposition. The U.S. is the largest ethanol producer in the world. In 2009, the U.S. produced 10.5 billion gallons of ethanol (seven billion gallons of gasoline equivalence) using corn as a feedstock while the second largest producer, Brazil, created about eight billion gallons of ethanol (5.5 billion gallons of gasoline) using sugarcane. Europe is the most important biodiesel producer in the market, with European rapeseed accounting for 58 percent of the global biodiesel produced in the world. Although biofuels have been a resounding success in Brazil where they displace 50 percent of gasoline consumption and do not use rainforest land, the U.S. and European experience has been more controversial. The “food vs. fuel” debate, land and water-use constraints, questions about whether the energy and carbon savings of biofuels are grossly overstated, and the reality that most forms of first-generation biofuels are uneconomical without generous government subsidies have tainted the perception that biofuels are a worthy alternative form of energy. The next few years will witness the commercialization of “advanced” biofuels. In 2010, the first commercial “cellulosic” ethanol plants will go online. Known as a “second-generation” technology, cellulosic ethanol is produced via bio-chemical or thermo-chemical means from the non-food component of biomass. The U.S. government has mandated that 100 million gallons of cellulosic biofuel be blended into the nation’s gasoline supply in 2010 increasing to 16 billion gallons in 2022. Large players like BP, Shell, Chevron, POET, ADM, INEOS, Abengoa and smaller companies (with large backing) like Coskata, Range Fuels, and Verenium are all relentlessly pursing cellulosic biofuel. Success for cellulosic biofuel producers will depend on many variables including: (1) access to consistent supply of affordable feedstocks, (2) ability to access project finance and/or government loan guarantees (3) improved economies of scale with production methods. While second-generation cellulosic ethanol remains a major priority among policy-makers and venture capitalists, serious attention is being paid to third-generation algae biofuels. Known as a “drop in” fuel, algae can potentially serve the gasoline, diesel, and aviation markets (whereas cellulosic ethanol only displaces gasoline). Certain strains of algae grow quickly and up to 60 percent of its body weight can be lipids, which are easy to transform into petroleum replacements. Algae consume CO2, can thrive in brackish or salt water, and do not require cropland. Although there are significant economic and logistical constraints affecting the commercialization of algae, this report provides an in-depth explanation of those constraints and the likelihood that unsubsidized algae will become cost competitive with petroleum prices.

This 307 page report provides a thorough examination of the liquid transportation market. Through understanding the key supply and demand side drivers for petroleum, we created oil price scenarios through 2019. Since biofuels are attempting to replace petroleum, any discussion about the future of biofuels must be grounded within the context of the economics of petroleum. We find that by 2015, cellulosic ethanol will be the largest “advanced” biofuel, comprising 2.4 billion gallons of the estimated 50 billion gallons of global biofuel produced. By 2022, algae biofuels are the largest biofuel category overall, accounting for 40 billion of the estimated 109 billion gallons of biofuels produced.

Key Elements of the Report:

Companies profiled include:Abengoa Bioenergy • Archer Daniels Midland • Cosan • Osage Bio Energy • Poet • Bunge/Diester Industrie • Neste Oil • Renewable Biofuels (RBF) • Biogasol • Bluefire Ethanol • Coskata • DuPont Danisco Cellulosic Ethanol (DDCE) • Enerkem • Fulcrum Bioenergy • Ineos Bio • Iogen • KL Energy • Mascoma • QTeros • Range Fuels • Vercipia Biofuels • Zeachem • Algenol Biofuels • Aurora Biofuels • Origin Oil • Petroalgae • Sapphire Energy • Solazyme • Solix Biofuels • Amyris Biotechnologies • Choren Industries • Cobalt Biofuels • Gevo • LS9 • Virent • Ceres • Edenspace • Genencor • ICM • Novozymes

|