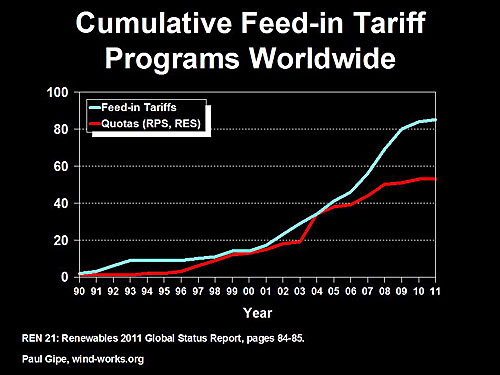

Snapshot of Feed-in Tariffs around the World in 2011Updated Tables of Feed-in Tariffs Worldwide Summary of Prices for Wind, Solar, Geothermal, & Other TechnologiesOct. 5, 2011 - Paul Gipe - wind-works.orgFeed-in tariffs are the world's most popular renewable energy policy mechanism. Despite the economic recession, more and more jurisdictions are turning to feed-in tariffs to spur not only renewable energy development but also industrial development and the attendant jobs that it creates. The following article is a snapshot of places where feed-in tariffs are being used, and the prices that are being paid. While extensive, this article is not comprehensive. It does not include every tariff for every technology in every jurisdiction, but it does give a flavor for the widespread use of this policy mechanism with the odd name. More than 80 jurisdictions around the world now use or have used feed-in tariffs to pay for new renewable generation, according to a recent report by REN 21. These vary from former Eastern Bloc countries, such as Slovenia and Bulgaria, to developing countries, such as Uganda and Mongolia, to the more well known examples of Germany and France. According to the Renewables 2011 Global Status Report, feed-in tariffs now dominate policy for renewable energy worldwide. There are 60% more jurisdictions (states, provinces, and entire countries) using feed-in tariffs than are now using quota systems (Renewable Portfolio Standards, Renewable Energy Standards, and so on).

Momentum for quota programs began leveling off in 2008 as the global recession first began to take hold. Even during the early years of the recession, however, momentum continued to build for feed-in tariff policies. Updated Tables of FITs Worldwide I try to maintain a multi-tab table (spreadsheet) of feed-in tariffs worldwide on my web site at www.wind-works.org. See Tables of Feed-In Tariffs Worldwide. I've recently updated the tables and now include current prices for Armenia, Austria, Belgium, Bulgaria, Cyprus, the Czech Republic, Denmark, Greece, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, Northern Indiana Public Service Company (NIPSCO), Nova Scotia, Spain, and Sri Lanka, as well as tariffs for numerous other countries. The full table is never complete or fully current, as the data changes frequently. For solar photovoltaics (solar PV), it changes even more frequently, as jurisdictions adjust their tariffs for new contracts to reflect falling panel prices. But the table remains one of the few such sources in the public domain. Most countries in the European Union (EU) now use feed-in tariffs as the policy of choice to develop their renewable resources. Earlier this year consultants to the EU released a major report on the status of member states' policies to meet their binding renewable energy targets. The 343-page report, Renewable Energy Country Policy Profiles 2011, includes extensive updates on feed-in tariffs in the member states. Much of the data in the report has been incorporated into my Tables of Feed-In Tariffs Worldwide. Price Alone is Insufficient For most, feed-in tariffs are solely about the fixed price paid for electricity produced by a renewable technology over a fixed term. And for many, unfortunately, this is only the price paid for solar PV. While a sufficient price is necessary for the rapid development of renewables, price alone is insufficient. Successful renewable energy policy requires a full suite of complimentary measures, most notably that access to the grid be quick, easy, and inexpensive. Most renewable energy advocates overlook the sub-title of Germany's Renewable Energy Sources Act: the "The Act on Granting Priority to Renewable Energy". The authors wanted to make the law's purpose and intent clear from the title alone, so there would be no ambiguity. They could have used deceptive euphemisms like those so popular on this side of the Atlantic, such as "The Full Employment and Jobs for Americans Act" to mask their intent. Instead, they wanted it to be clear to all stakeholders, and to their parliamentary colleagues, that the law required that renewables be given the "right to connect", and the "right to sell electricity to the grid" as well as priority over electricity from fossil-fired and nuclear generation. The success of the German program is as much about the right to connect and to sell electricity as it is about the specific payment per kilowatt-hour for each technology. Nevertheless, without a price that permits profitable development no one will build renewable generation and connect to the grid. Price remains critical, and for that reason, I've summarized below some of the prices paid--the tariffs--for various technologies during the first year of operation. Renewable Tariffs & Heritage Resources The tariffs in the following tables are arranged from the highest to the lowest and are not sorted alphabetically. The reason for this is to help the reader gain a quick grasp of what is being paid for a particular technology around the world. Consequently, it is important to note the difference between these posted prices and the price of generation from "heritage", or existing, sources. In most cases, renewable tariffs are higher than those of heritage resources. There's good reason for this. Renewable tariffs pay only for new generation. The capital cost of heritage sources have often, if not nearly always, already been recovered--some many times over. Thus, the price paid for heritage generation is very low in comparison to the price needed to pay for electricity from newly installed generators like a new nuclear plant, a new coal plant, or a new wind plant. This distinction is often lost on policymakers and even on some in the electric utility industry and its regulators. Contract Term Best practice worldwide is to offer contracts for a period, or term, of 20 to 25 years. Some jurisdictions are successful with terms of 15 years. Some, such as Ontario, offer terms of as much as 40 years for long-lived technologies such as hydro. Longer contract terms lower the initial price necessary for the same level of profitability. Thus, longer contract terms may be more politically palatable, especially in North America where the price from heritage resources is so low.

However, longer contract terms increase the risk from inflation. Some mistakenly believe that inflation only affects the operations and maintenance side of the profitability equation, or the cost of fuel for biomass and biogas plants. Inflation affects the real rate of return that an investor can expect from the equity or capital invested in a project. Inflation erodes the real rate of return over time and as the time period becomes longer, the risk increases. For this reason many programs include inflation protection to cover a portion of this risk. Inflation Adjustments If productivity is determined by the resource, and all other factors remain the same, then profitability is determined by the tariff and the inflation adjustment. To improve profitability, the price can be increased, or the inflation adjustment can be increased, or some combination of the two can be used. In no case can the tariff be lowered and the inflation index lowered at the same time without hurting profitability. To maintain profitability when the tariff is lowered, the inflation index must be increased to compensate. Programs in Germany and Spain represent two extremes in how they respond to inflation. Germany's Renewable Energy Sources Act does not account for inflation outside the contract. In the early Spanish program, tariffs increased annually 100% with the inflation in electricity prices under the fixed-tariff option. This feature was built into the program because Spanish renewable tariffs were calculated as a fixed percentage of the "Average Electricity Tariff" determined annually. (This system has since been changed.) Most programs fall somewhere in between these two extremes. France includes both an adjustment in the base tariff for inflation, and, within a contract, an adjustment of the contracted tariff. Once the contract has begun, the tariff paid increases with 60% to 70% of inflation.

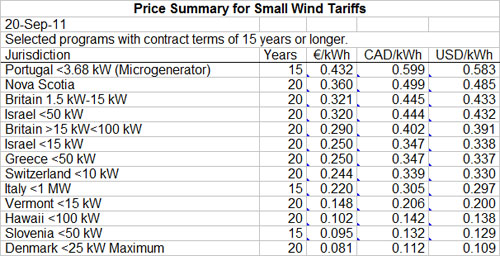

First Year Price The design of feed-in tariffs can be as flexible and as complex as policymakers desire. Consequently, it is very difficult to summarize worldwide tariffs for a particular technology with a single entry.The "first-year price" shown in the following tables is just a snapshot of the tariffs for a particular technology in a particular jurisdiction. Best practice worldwide is to provide tariffs that are differentiated not only by technology but also by size, application, and, in some cases, by resource intensity. For example, there are six different tariffs for solar PV in Ontario and twelve different tariffs in Germany. One could sort the tariffs for a particular technology, for example solar PV, by size and application. Unfortunately, that would make this article even longer than it already is. Further, the price or tariff paid during the first year may not accurately reflect what will be paid during the full duration of a feed-in tariff contract. This is particularly true where tariffs are adjusted for resource intensity after several years of operation. For example, wind energy tariffs in Germany, France, and Switzerland can be reduced in later years depending upon a measure of the productivity of the wind resource. Lowering the tariffs in later years cuts the average price paid over the full contract term relative to the initial price shown in the tables. Keep these caveats in mind when reading the following tables. Small Wind Tariffs While they are not as well known as solar PV tariffs, there is an increasing number of policies paying specific tariffs for electricity generated by small wind turbines. In September, Nova Scotia launched its ComFIT program, which features one of the world's highest tariffs for generation from small wind turbines. The following table lists only one entry for Great Britain. However, Britain offers four different tariffs for small wind turbines and two tariffs for medium-size wind turbines. Small wind development is now proceeding apace in Great Britain and Italy. Since Britain's feed-in tariff program was begun in the spring of 2010, small wind generating capacity has more than doubled.

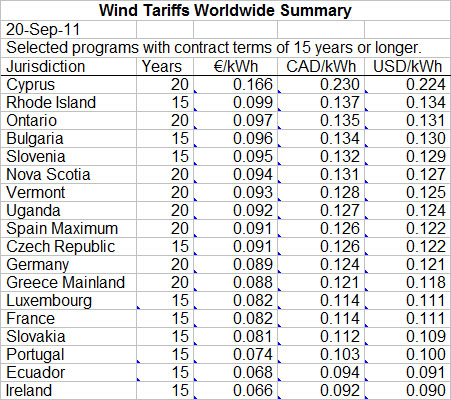

Wind Tariffs Tariff levels are a function of resource intensity for all technologies, but more so for wind energy than for any other technology. The power in the wind is a cubic function of wind speed. Slight changes in average annual wind speed from one site to the next can have a profound effect on the amount of electricity that a wind turbine can produce. As a consequence, the tariff necessary for profitably operating a wind turbine on the windswept west coast of Ireland is far lower than that for mid-continent sites like those in Ontario, Canada. Tariff levels may also reflect the type of application envisioned by policymakers. Nova Scotia's tariff is applicable only to wind turbines that are community owned. To qualify for the tariffs in Rhode Island and Vermont, wind developers are restricted to effectively one wind turbine. Wind energy is more expensive when produced by one wind turbine than by a cluster of turbines or a small wind farm, because costs of operation and maintenance can be spread across more wind turbines. Thus, programs limiting feed-in tariffs for wind energy to only one turbine will of necessity pay higher prices for the same wind resource than programs allowing greater installed capacity.

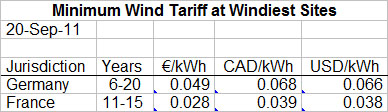

As noted previously, a simple summary of first-year tariffs across jurisdictions may not capture program subtleties, such as tariffs that vary with resource intensity. Wind tariffs in Germany, France, and Switzerland vary by resource intensity. In all three countries, electricity from wind turbines is paid a fixed price--the price listed in the table above--during an initial or trial period. After this period (five years in Germany and Switzerland, ten years in France), the tariff may change. In Germany and Switzerland the base tariff is extended by a specified number of months after the trial period, when the productivity of the turbines is less than the target; that is, if the site is less windy than that used in the tariff calculations. At a windy site in Germany, after year five the tariff falls to the value listed in the table below. In France, after year ten, the tariff is adjusted based on the productivity of the turbine. Thus, in Germany, France, and Switzerland the time-weighted average tariff for wind energy is less than the first-year tariff. Sometimes the time-weighted equivalent tariff is much less than the first-year tariff. It is for this reason that the cost of wind energy to ratepayers in these countries is not simply the product of the terawatt-hours produced times the posted tariff. This subtlety is not only lost on many politicians but also on many renewable energy advocates.

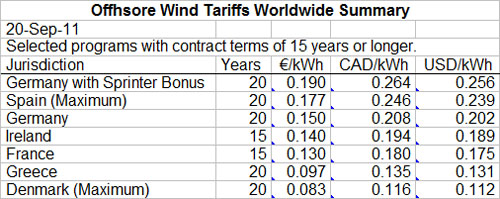

Tariffs differentiated by resource intensity are not limited to wind energy. For a brief period France employed feed-in tariffs for solar PV that differed by insolation. Sites in cloudy northern France were paid a higher price for solar-generated electricity than sites along the sunny Riviera. Offshore Wind Tariffs As noted in the section above, the tariffs for offshore wind energy in Germany and France vary by resource intensity. The table below lists only the first-year tariff.

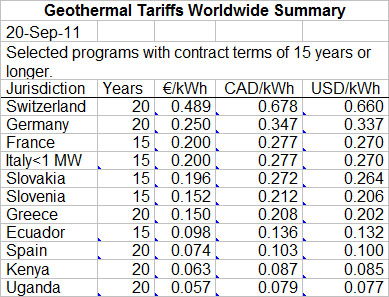

Geothermal Tariffs Outside of Italy, there's very little geothermal development in continental Europe. There's especially little experience with small geothermal projects in the 10 MW to 20 MW range. Thus, the tariffs below are based on limited experience and intended to pay for the high costs of early high-risk projects. See Geothermal Feed-in Tariffs Worldwide for more on geothermal tariffs.

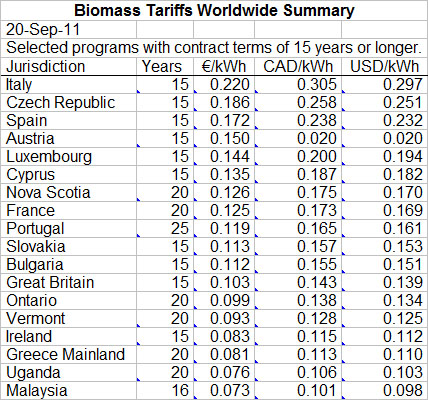

Biomass Tariffs Biomass tariffs are as complex as the other technologies. Each jurisdiction defines biomass differently. Some include biogas under biomass. Others list them separately. Most jurisdictions vary tariffs by project size. Some also vary the tariff by fuel source and even the percentage of various fuel sources used. The table below is only a gross approximation. For details see the listing for each individual jurisdiction in Tables of Feed-In Tariffs Worldwide

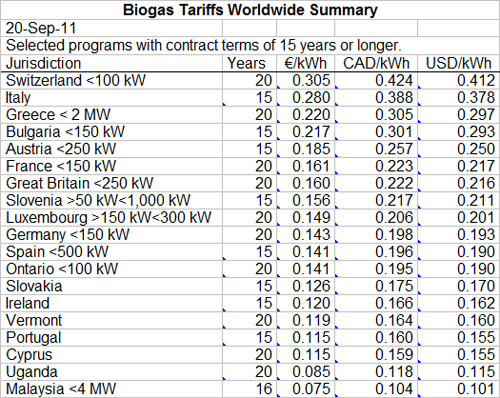

Biogas Tariffs Biogas may include landfill gas, sewage treatment plant gas, gas from farm wastes (manure), or gas from a host of other sources. Some jurisdictions lump these sources together, others calculate a separate tariff for each while also varying the tariff by project size. For example, Ontario offers five tariffs for biogas depending upon project size. Germany and France offer separate tariffs for landfill gas, sewage gas, and gas from on-farm anaerobic decomposition.

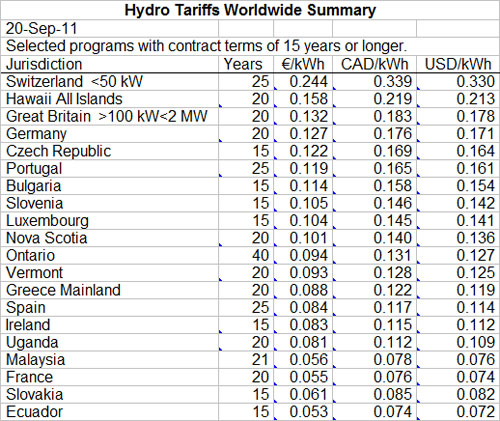

Hydro Tariffs Most feed-in tariffs for hydroelectric generation are limited to "small" hydro or run-of-the-river hydro. In many jurisdictions, large hydro is restricted to state enterprises, as sites for large projects are extremely limited. As with other technologies, most hydro tariffs vary by project size. The summary below is just a snapshot of first-year tariffs for the smallest projects.

Wave & Tidal Tariffs As with continental European geothermal energy use outside Italy, tariffs for wave and tidal generation are based on very limited data and practically no real-world experience. Thus, the tariffs below are conjecture on what projects might need if built. As projects come on line and experience is gained from operation, the tariffs could be decreased for new projects over time. Portugal specifically limits its tariffs for wave generation to the first plants in each size category. Interestingly, Nova Scotia defended its decision not to include solar PV in its ComFIT program by noting that solar PV was "immature". Yet Nova Scotia proceeded to offer the world's highest tariff for "immature" tidal power.

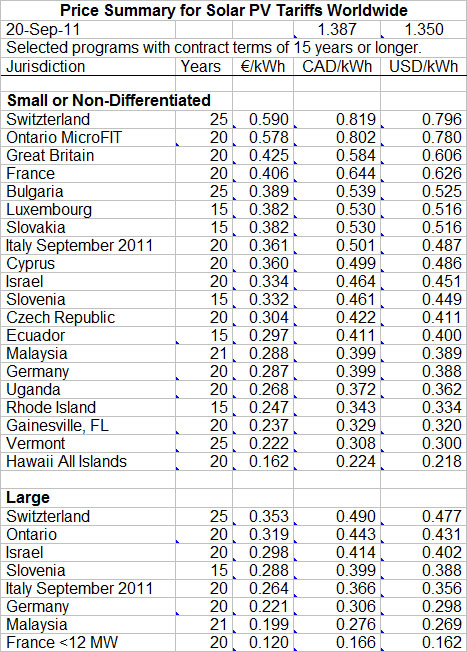

Solar PV Tariffs In many jurisdictions, tariffs for solar PV vary by application (rooftop or groundmounted) and by size. As noted previously, there are six different tariffs for solar PV in Ontario and twelve different tariffs in Germany. In 2010, solar PV tariffs in France for projects greater than 250 kW varied by département from a base rate representing the sunny Riviera to a high of 1.2 times the base rate for cloudy northern France along the Belgian border. In the following table, the first set of tariffs represents small rooftop systems. The second portion represents large groundmounted systems. First-year tariffs for solar PV in Italy during 2011 decrease--degress--by month. The value for September is shown below.

Summary of Heat Tariffs Tariffs for heat are not included in this snapshot. Though Luxembourg, for example, pays a tariff for commercial heat from biogas or solid biomass of €0.03/kWh (~$0.04/kWh), there is no summary table of heat incentives in this snapshot. The tariff is included in the table for Luxembourg and will be included in a future article summarizing renewable heat tariffs. More Information Needed More detail on the tariffs in a number of countries is needed to keep Tables of Feed-in Tariffs up-to-date. While there are reports of feed-in tariffs in Nicaragua and Honduras, I have not found any specific information. Similarly, my information is incomplete on Sri Lanka, Moldova, and Armenia, to name only a few. -End- |