Top 10 US states offer more than 40GW of solar PV pipeline capacity

Jan 14, 2014 - Michael Barker - pv-tech.org

At the end of 2013, based on annual market demand, the top 10 states for solar PV in the US had an aggregate project pipeline of approximately 2,000 non-residential projects. This represents almost 40GW of potential PV capacity.

Project pipelines provide significant insight into individual projects, but also help understand market structures, business models, and future demand levels.

|

|

|

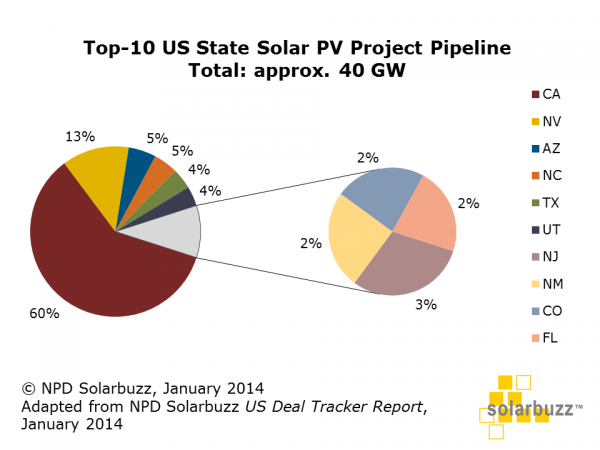

Figure 1: The top 10 US states currently have a non-residential solar PV pipeline of approximately 40GW. Source: NPD Solarbuzz United States Deal Tracker.

|

|

|

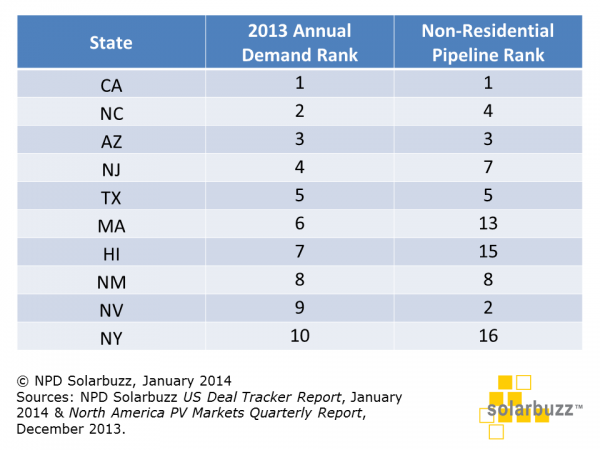

Figure 2: Top 10 US States by 2013 demand, with non-residential pipeline ranking status. Source: NPD Solarbuzz North America PV Markets Quarterly and United States Deal Tracker.

|

Figure 1, to the left, shows the total project pipeline levels (all projects yet to be completed), for the top 10 US states, based on total pipeline capacity.

California dominates the 40GW pipeline, with over 60% of capacity, firmly cementing its place as the leading US market. In fact, if California alone was compared on a global level, it would have ranked as the fourth largest global PV market in 2013.

By examining where states are ranked – in terms of pipeline capacity – long-term demand trends can be established. States with smaller pipeline levels may be in danger of declining year on year, as project development activity slows down and current pipeline activity gets depleted.

Conversely, states that rank higher, in terms of project pipelines, may see strong demand growth in the coming years as projects start to be completed.

However, it is worth pointing out that the pipeline relates only to non-residential (commercial/utility) solar PV installations. Therefore, states that have strong residential segments, such as Hawaii, may have smaller non-residential pipeline capacity but retain strong PV ranking status by virtue of residential activity.

Regardless of where individual states rank, in terms of market or pipeline size, the US market offers tremendous long-term growth opportunities. Any PV company (manufacturer, installer or developer) that wants to participate on a global level clearly needs to have a strategy for the US market; within this, it is essential to understand the size of state markets today and also the strength of the project pipelines driving PV demand going forward.

Co-authored with Christine Beadle, downstream market analyst for NPD Solarbuzz

|