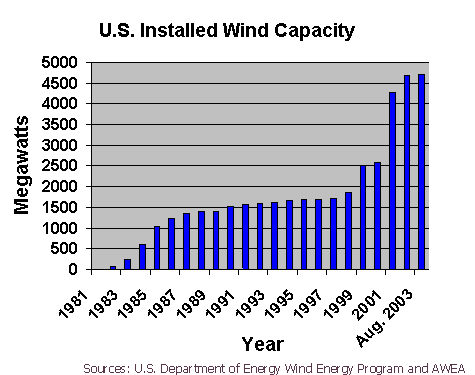

Policy Options: TaxesA case study of production tax credits in the United StatesThe United States' production tax credit is available for wind, closed-loop biomass and poultry waste. The policy provides a $.015/kWh credit to all operators of renewable energy facilities" (AWEA). The credit is ideally set at a level that makes it more cost effective to produce electricity from renewable resources than from fossil fuels. This tax incentive significantly helped boost wind power development in the last decade. Wind power has always faced an obstacle in the US because utilities pay artificially low energy prices to Independent Power Producers (IPP). Utilities can pay IPPs for their energy to avoid the cost of producing it themselves. The price of natural gas, at $0.02 to $0.035 per kWh has been the accepted amount utilities pay IPPs for energy. The PTC set wind's price at $0.19 (adjusted for inflation), making wind development projects economically attractive. In addition, total project revenue is now $0.05 per kWh, adding to the profitability of wind projects.

The US energy production tax credit was originally created in the Energy Policy Act of 1992. The Economic Security and Recovery Act of 2001 extended the credit until December 31, 2003. The PTC has provided incentive for approximately $5 billion in capital investments to wind energy projects in the US and has directly led to major improvements in equipment reliability. Equipment efficiency and reliability is perhaps an unintended, yet highly beneficial, result of the PTC. The most efficient turbines with higher production capacity and lower management costs are more likely to be considered for a project utilizing the PTC This is due to the considerable competition between manufacturers exists to sell power to utilities and because manufacturers reimburse the owner for lost revenue due to inefficiency. Utilities can chose the turbines that will produce power more of the time. Consequently, the risk is now minimal for the project finance community. (World Link Insurance) The Union of Concerned Scientists reports that production tax credits are more effective when they are implemented in conjunction with policy that creates a market for renewables. A Renewable Portfolio Standard is one such policy driver to increase market demand for electricity generated from renewable energy. The Union of Concerned Scientists found that wind capacity increased most in states with a state RPS. The disadvantage of production tax credits is the uncertainty as to when the law will be repealed. When there is no longer a credit, the company doesn't receive compensation, and it may no longer be profitable to produce electricity from renewable resources. Therefore, producers can decide to not get into the market of renewables with the risk of producing an unprofitable good in the future. (The Bureau of National Affairs, Inc.) |